Updates To CPF Usages & HDB Loans For Old Flats

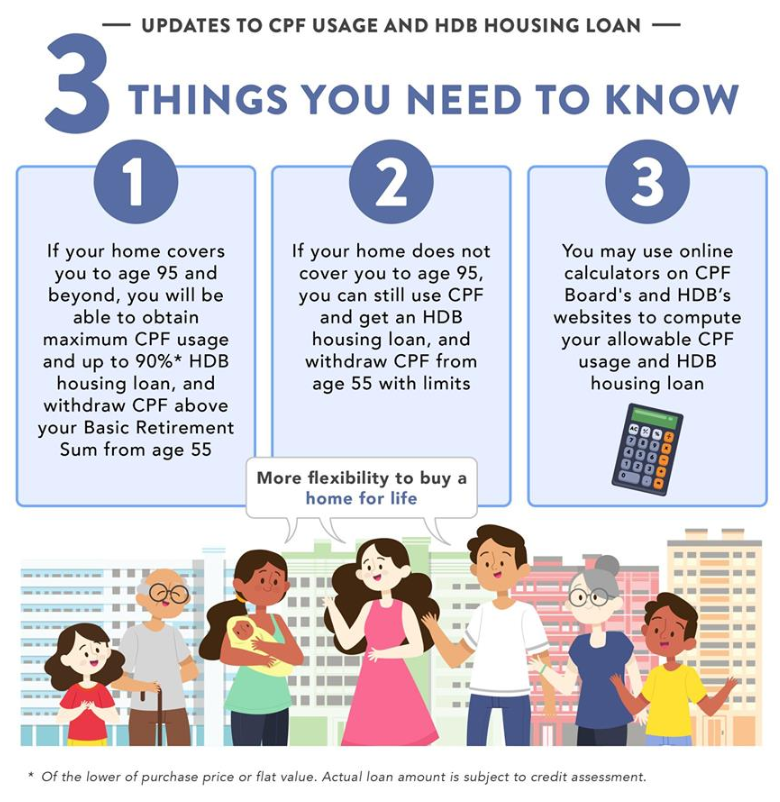

From 10th May 2019, CPF – Central Provident Fund rules will be updated to allow buyers of older HDB flats to use more CPF, so long as the lease can cover the home-owners until they are at least 95 years old.

Likewise, HDB will be updating its housing loan rules so that buyers of such flats will be entitled to the maximum loan quantum.

Those who do not meet the lease coverage will still be allowed to use CPF and take up HDB housing loans, but at a pro-rated amount to safeguard their retirement adequacy.

The updated rules will provide more flexibility for Singaporeans to buy a home for life, and will apply to both public and private properties.

Source: MOM (Facebook)

.

Instead of focusing on the remaining lease of a flat previously, the new rules will now look at if the balance leases can cover buyers until the age of 95 years old.

A minimum lease requirement will still apply.

HDB flats must have at least 20 years left on their leases (previously is a minimum of 30 years) in order for buyers to use their CPF for the purchase.

CPF members aged 55 years or older will also need to have properties with leases covering them until age 95 (instead of a remainder of at least 30 years) before they can withdraw their CPF savings in excess of the Basic Retirement Sum (BRS).

.

Here are two examples of how the new changes will affect buyers:

Source: MOM (Facebook)

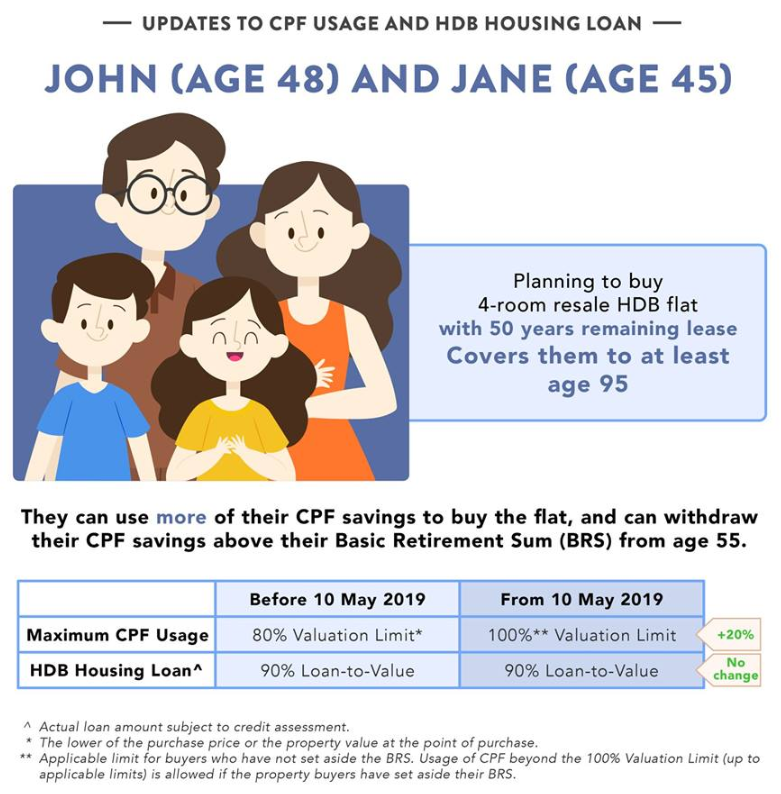

John, 48, and Jane, 45, want to buy a four-room HDB resale flat that costs S$430,000 with 50 years remaining on its lease. The lease will cover the youngest buyer, 45-year-old Jane, until age 95.

Under the existing regulations, they can use their CPF savings for up to 80 per cent of the property’s valuation limit, which amounts to $344,000. The valuation limit is the lower of the purchase price or the value of the HDB flat at the time of purchase.

The couple can also take a HDB loan of up to 90 per cent of the property’s value, which translates to S$387,000.

Following the changes, the couple can tap on their CPF for up to 100 per cent of the property’s valuation limit (S$430,000, or up to S$86,000 more than before), if they have not set aside the Basic Retirement Sum. There is no change to their HDB loan cap.

.

Source: MOM (Facebook)

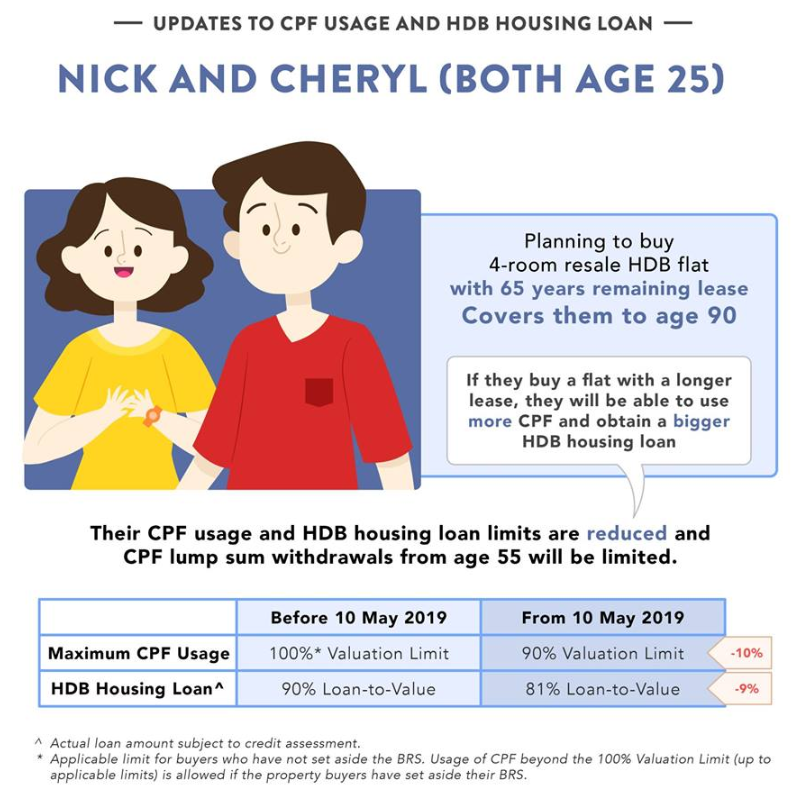

Nick and Cheryl, both 25, want to buy a four-room HDB resale flat that costs S$430,000 with 65 years remaining on its lease. The lease will not cover the couple until age 95.

Under the existing regulations, they can use their CPF savings for up to 100 per cent of the property’s valuation limit as the lease of the flat exceeds 60 years. They can take a HDB loan of up to 90 per cent of the property’s value, which amounts to $387,000.

Following the changes, the couple can tap their CPF for up to 90 per cent of the property’s valuation limit (S$387,000, or S$43,000 less than before). Their HDB loan cap is reduced to 81 per cent (S$348,300, or S$38,700 less than before).

.

As reported, majority of Singaporeans will not be affected by the changes, said the ministries on Thursday.

98% of all HDB households have homes that will cover them until age 95 or beyond, while for private property households, the proportion is 99 per cent.

.

For more details, please refer to the following sources:

For CPF, click HERE.

For HDB, click HERE.

Information Source: CPF, HDB, MND, MOM and Various Online News Sources